Now that all major publicly-traded health insurers have reported earnings for the second quarter, the verdict is clear: this is a challenging year for managers of risk.

I’ve previously written about some of the mega-trends driving healthcare spending in the U.S. over the past forty years, and some of these trends are at play in this year’s turbulence. To get a handle on recent developments, I sifted through the latest round of quarterly earnings reports and analyst call transcripts for 9 health insurance companies, looking for signals on the types of care that are growing faster than carriers expected and therefore weren’t fully accounted for when plans were locked and prices were set.

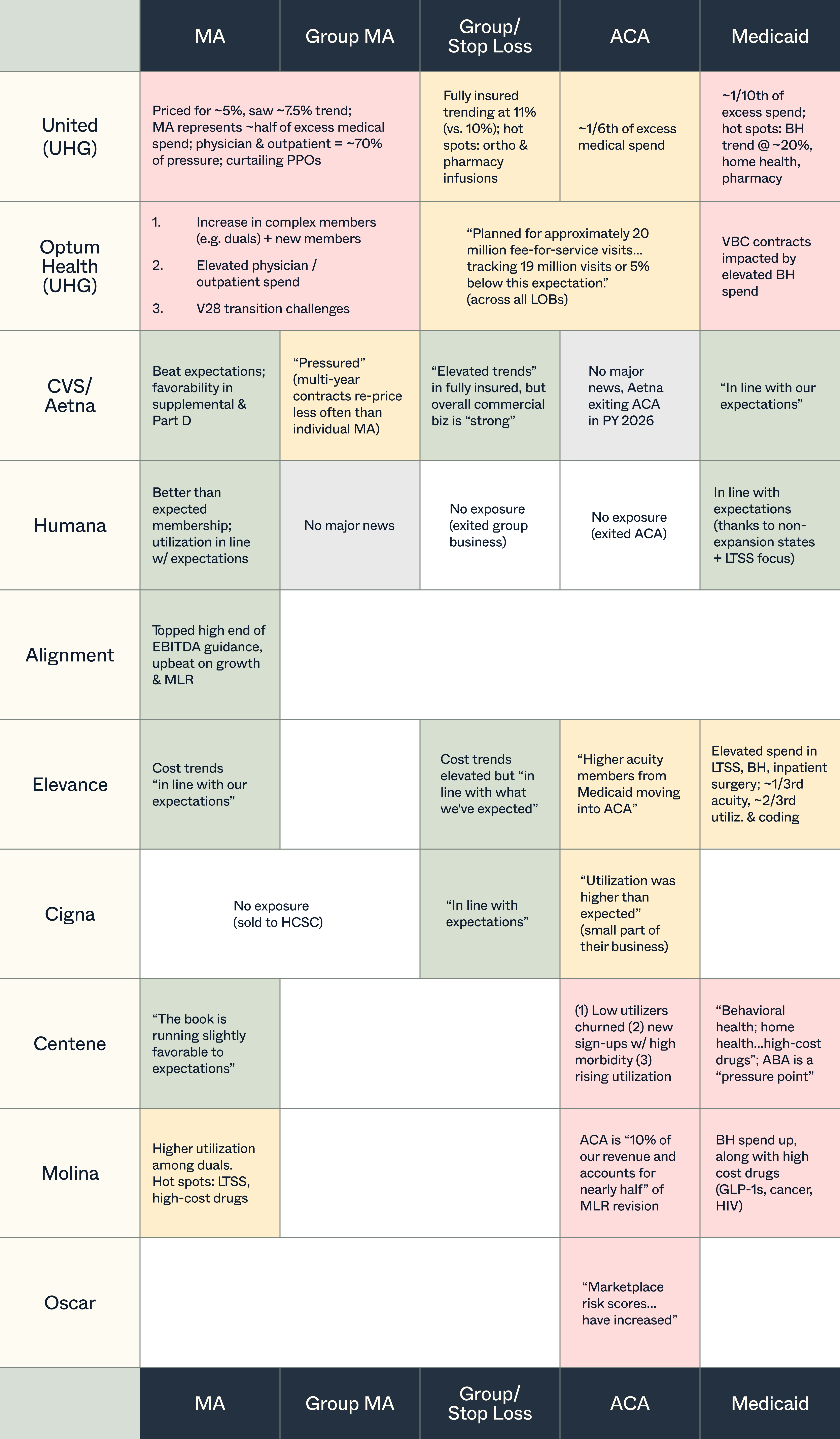

While all lines of business across all carriers (with few exceptions) are showing signs of elevated utilization, there are market-specific nuances to unpack:

- In Medicare Advantage, the roll-out of v28, which reduced risk adjustment payments, has forced a trade-off between price, plan richness, and profitability; many of the large MA players shared that they anticipated the headwinds in pricing this past AEP. Meanwhile, VBC groups with Medicare Advantage exposure (including Optum Health) have to absorb cost spikes without the power to re-price. It bears mentioning that this is a setback in what has otherwise been a 15-year bull run for Medicare Advantage carriers.

- Nearly all payors are battling medical cost dislocation in the ACA (even before subsidy expiration takes effect). If you extrapolate from Centene’s experience, it’s due to a combination of underlying utilization increases as well as low-utilizers leaving the market this OE, plus a crop of higher acuity first-time enrollees (as a counterpoint, Oscar shared that its proportion of low-to-no utilizers didn’t change much). Interestingly, some payors pointed to the shift of Medicaid members into the ACA as a headwind for Medicaid, others as a headwind for the ACA.

- In Medicaid, the key utilization trends were: behavioral health (ABA was called out specifically by one carrier), home health, and drug costs with one mention of surgery spend. Across the board, there are efforts underway to re-negotiate the capitated reimbursement MCOs get from states, which were set based on now outdated utilization assumptions.

- Centene’s CEO offered an additional perspective on what could be behind the uptick in utilization in its two main markets, beyond the other factors mentioned: “from a behavioral economics standpoint…[if] you think about Marketplace and Medicaid members, what these folks have been hearing from every major media outlet for the last six months is that Congress is going to take away their health insurance. And that I think does drive a certain level of behavior when compounded with macroeconomic uncertainty.”

- In the group market, fewer details were shared on underlying cost drivers, but UHG highlighted orthopedic care and pharmacy infusions (the relatively positive news on employer performance hints at a turning tide after a quarter or two of disruption in group and stop loss markets late last year).

Despite the current rockiness, most payors struck a cautiously upbeat tone in talking about the journey back to business stability, between cost-cutting initiatives (enabled in part by AI) and the opportunity to re-price premiums or narrow networks to better reflect new market realities.

In Medicaid specifically, if the Centene theory bears out and members have indeed been front-loading care in anticipation of losing coverage, next year may bring lower than expected utilization and with it a partial reversal of fortunes.

For healthcare founders selling into payors, in the very near-term, tightening budgets can mean stalled sales cycles. But, these trends can also become fertile ground, with opportunities on both the provider and the payor side to ensure care is reimbursed appropriately and delivered cost-effectively.